Consumer shopping activity on comparison shopping websites increased dramatically starting in mid-March and continued at a brisk pace into May and June, according to Jornaya and Equifax. (Provided image)

Consumer shopping activity on comparison shopping websites increased dramatically starting in mid-March and continued at a brisk pace into May and June, according to Jornaya and Equifax. (Provided image)Equifax’s auto insurance shopping statistics for the first half of 2020 indicate that globally, shopping activity declined during the first few months of the pandemic when compared to January levels, then recovering in June, as the graphic above illustrates. However, as with anything in the auto insurance industry, to understand what’s truly been going on with consumer and carrier/agent behavior, it’s all about one word: Segmentation.

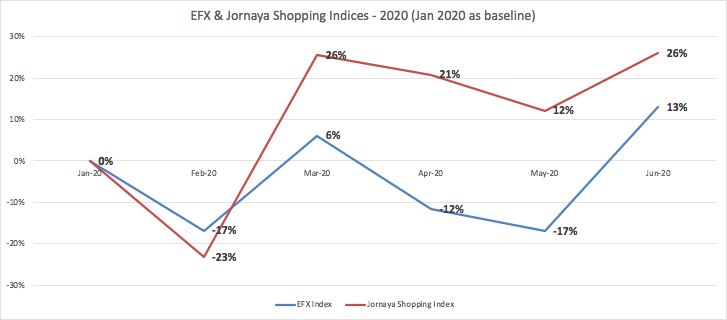

At Jornaya, when we segment the auto insurance shopping activity and shine a spotlight on a meaningful source of auto insurance consumer prospects for agents and carriers —comparison shopping websites — there’s a much different narrative. Now, we could point to the increase in internet usage as the analogy, but that’s less interesting than something like alcohol sales. The point: Consumer shopping activity on comparison shopping websites increased dramatically starting in mid-March and continued at a brisk pace into May and June, where YOY increases were 41% and 68%, respectively.

So what does Meat Loaf (the rock ‘n’ roller, not the dish) have to do with all of this?! What we have witnessed from the performance marketing ecosystem in terms of shopping volume reminds us of one of the best-selling albums of all time by a singer-songwriter who took his entertainment moniker from a popular baked beef dish. You guessed it: Meat Loaf. In mid-March, auto insurance comparison shopping activity took off like a “Bat Out of Hell.”

Global shopping activity

Equifax Auto Insurance Inquiries are utilized by auto insurance companies when a consumer is near the end of a shopping journey — signaling the consumer has finished an application and is ready to purchase a policy. Companies request an auto insurance inquiry as part of the process to finalize the quote prior to a consumer purchasing a policy. Equifax generates millions (and growing) of all auto insurance inquiries/quotes/bind decision in the marketplace every month, so its inquiries serve as a solid proxy for global auto insurance shopping activity that takes place near, what many refer to as, the bottom of the shopping funnel when a consumer makes the final purchase decision.

The graphic above illustrates the monthly trend in Auto Insurance Inquiries Equifax provided to companies during the first half of this year, with January 2020 serving as the baseline for subsequent months. After a 6% increase in March, Equifax experienced a decline in inquiries in April and May and then rebounded in June at a level 13% higher than January.

Comparison shopping activity

With its technology embedded on nearly every insurance comparison shopping website, Jornaya witnesses, among other personal insurance products, auto insurance activity that takes place across most of the shopping funnel. For over two decades, consumers have visited these comparison shopping websites to fill out one quote form and then proceed to interact with carriers and agents to receive multiple auto insurance quotes. It is this activity that feeds Auto Insurance Inquiries that Equifax provides after the consumer visits a comparison-shopping website. Inquiries resulting from comparison shopping make up only a fraction of the total quotes generated (some have estimated about 1 in 5), with the majority of inquiries coming from consumers working directly with carriers and agents.

In recent months, we estimate comparison shopping represented a higher than usual amount of total activity and remains a meaningful source of new auto insurance business for agents and carriers. For example, in the first half of 2020, Jornaya witnessed millions of auto insurance shopping events every month at a rate of 1.58 auto insurance shopping events per unique consumer.

Our graphic illustrates Jornaya’s index dropped slightly more than the Equifax index in February, but then shot up significantly above it in March and remained higher through June (when the gap starts to narrow). Consequently, the auto insurance comparison shopping path to obtaining quotes from agents and carriers began to widen starting in March.

Key drivers and undercurrents

To understand what fueled the increased comparison shopping activity, one needs to look no further than the impacts the pandemic has had on consumer and agent/carrier behavior.

- Unemployment: According to the Bureau of Labor Statistics, job losses started in March and then plunged by historical amounts in April (over 22 million combined in March/April). Even with job gains in May and June of over 7 million, unemployment remained at 11.1% in June. Consumers facing financial uncertainty likely turned to seek ways to reduce household expenses, including the cost of car insurance.

- Stay-at-home: As Americans migrated, almost overnight, to working at home starting in mid-March, many had more time available (and fewer at-work distractions) to seek ways to reduce household essential and non-essential expenses. And don’t forget, like consumers, local agents staying at home were not out in the community doing what they do best: aggressively engaging with prospective customers and stimulating shopping activity.

- Federal Reserve interest rate cuts: In March, the Fed twice cut interest rates by a total of 150 basis points, causing mortgage rates to decline. Consumers, in expense reduction mode, flocked to lenders, and mortgage refinancing surged starting in March. What does this have to do with auto insurance shopping? Keep reading…

- Premium rebates/credits: Auto insurance carriers started issuing premium rebates/credits in early April. This unprecedented action by carriers may have caused a “consumer awakening” and “shop and save” initiative by consumers. A recent J.D. Power survey found consumers were nearly twice as likely to shop if there’s a rebate or credit offer.

- Carrier advertising: Broadly, ad spending is expected to drop by 13% this year. While first-half 2020 auto insurance advertising data is not yet available, we believe overall spending on traditional forms of advertising fell significantly. As live sporting events vanished, so too did the ad inventory for auto insurance companies. Furthermore, for ads that did appear, the messaging seemingly shifted as a result of the pandemic impacts (e.g., less “shop and save” and more “premium rebates/credits” and “you’re not alone… We’re in this together” themed advertising).

Insurance performance marketing

Performance marketers who own insurance comparison shopping websites are some of the best digital marketers around. These companies have worked tirelessly since the late 1990s to build an efficient and effective technology ecosystem that connects consumers with agents and carriers. Because local agents were sitting at home and carriers were advertising less, there has been significant excess sales capacity.

This has all taken place during a time when carriers were properly priced and seeking growth. As a result, agents and carriers have shifted more advertising budget to purchase insurance leads and calls generated by comparison shopping websites. We have also heard that since mid-March, many more insurance agents have signed up to purchase leads and calls for the first time ever. With consumer interest and agent/carrier demand high, performance marketing companies literally scaled overnight to meet it.

The impact of interest rate cuts

At Jornaya, we call this the “mortgage dynamic.” Jornaya also witnesses the vast majority of all mortgage comparison shopping activity (e.g., Purchase, Refi, HELOC, Reverse). When the Fed cut interest rates by 150 basis points, lenders became flooded with organic inbound traffic/inquiries to their own first-party websites and call centers. Unlike auto insurance providers, lenders didn’t have enough capacity to handle the surge. As a result, lenders significantly reduced spending on mortgage leads from comparison shopping websites. In the second week of March, we saw lender demand for leads fall (by half of January/February levels), and this demand, while recovering somewhat in June, has remained relatively slow since — particularly given mortgage rates have hit historical lows. Diversified performance marketing companies (i.e., operating both insurance and mortgage comparison shopping sites) recognized this drop in demand immediately and, given the increased demand for insurance leads/calls, shifted ad spend over to insurance thus driving incremental comparison shopping activity.

What’s next?

We do not expect the consumer “shopping for savings” spree nor demand for new business from agents and carriers to slow down anytime soon, and certainly not for the remainder of the year (but for the normal big holidays).

Because of a variety of factors such as economic uncertainty, high unemployment, less driving and significantly higher household savings rates, consumers will continue to seek ways to reduce expenses on major household expense items, including auto insurance. Premium rebates/credits and rate reductions will add further incentive for consumers to shop around.

We’ll keep an eye on things and report back to the market periodically with updates and outlook. We also plan to drill into other important segmentation items such as home insurance shopping trends (in relation to auto), shifts in the risk spectrum distribution (e.g., whether normally shy preferred consumers are shopping at higher levels than normal) and geography.

While price comparison websites helping to connect consumers with carriers and agents have been a meaningful part of the auto insurance shopping ecosystem for several decades, their importance has never been greater. We don’t see that changing anytime soon either, so segmenting the global shopping activity will continue to be important in order to understand where and how consumers are shopping and to avoid missed growth opportunities in an extremely competitive environment.

Jaimie Pickles ([email protected]) is general manager of insurance at Jornaya. Kevin Leslie ([email protected]) is senior marketing officer for insurance at Equifax. David Dou ([email protected]) is a data scientist at Equifax.

See also:

"auto" - Google News

August 24, 2020 at 08:49PM

https://ift.tt/34t65Os

Alcohol, Meat Loaf and auto insurance comparison shopping - PropertyCasualty360

"auto" - Google News

https://ift.tt/2Xb9Q5a

https://ift.tt/2SvsFPt

Bagikan Berita Ini

0 Response to "Alcohol, Meat Loaf and auto insurance comparison shopping - PropertyCasualty360"

Post a Comment